America Turns 250. Its Biggest Companies Never Do—And That's Great!

AI is speeding up business turnover, which is exactly what the US is optimized for

Numbers are generally as of July 1st, 2026.

Tomorrow, the United States turns 250. I wasn’t planning on writing a birthday piece, but the mood suddenly struck me, especially as I reflected on what makes America unique.

Three weeks ago, a company founded in 2002 went public in the largest IPO in history and became America’s sixth most valuable company. This, of course, is SpaceX. Depending on the day and time, it’s also the sixth most valuable company in the world—trading off against TSMC. This is because all five companies above it are American.

SpaceX is obviously young, but the other five are also young(ish). Nvidia, Alphabet (Google), Apple, Microsoft, and Amazon. Sure, they’re not “a few years old” anymore, but they also aren’t generational companies from the turn of the century either.

The oldest is Microsoft, founded in 1975.

As Europeans would tell you, that’s basically no time at all. The biggest European company is ASML, which is also relatively young… but the next tier includes Roche, HSBC, Novartis, and AstraZeneca—founded in 1896, 1865, and (the latter two) via 1990s mergers of drugmakers dating back to the 1700s and 1800s. Following those are LVMH (1987, but with houses going back to 1743), Nestlé (1866), and Siemens (1847). SAP, young(ish) as well, used to be on this list, but then SaaSpocalypse happened.

Europe is obviously part of “The Old World.” The US is 250 years old. It’s still a “young” country in a way… but not that young anymore. It genuinely does turn over companies relatively rapidly.

Not that this is a surprise, but new firms displacing old ones is essentially how we generate all sustained economic growth—and hence improvements in human welfare. Last October, the Nobel committee gave the 2025 economics prize to Joel Mokyr, Philippe Aghion, and Peter Howitt for the economics of “creative destruction,” their work helping to elucidate the mechanics of this process.

And every few weeks, Torsten Slok at Apollo publishes yet another chart showing business creation in America at the highest rate ever recorded.

The Boom, and What It Is and Isn’t

Not to make Slok the star of this piece, but he’s got some great charts on this phenomenon, early as it is.

His interpretation: the boom is “being fueled by AI and large language models, which are dramatically reducing the cost and complexity of launching a company.” I’d agree, though some of the differential is driven by industries more open to technological adoption in general, not just AI.

Of course, this has been happening for a long time. Software, for example, has relentlessly driven down the cost of business until it was fairly minor even before AI. Writing software used to require room-scale mainframes and punch cards. Even in the era of the PC, it still required putting monumental effort into ensuring a final product was created before it could be shipped out with floppy drives and later CDs. Then, even after the online era arrived, companies needed to manage a bunch of physical servers and painfully set up early routers to connect to the nascent Internet (which was slow enough that a lot of software was still mailed). Finally, the SaaS (software-as-a-service) with always-online software arrived, which took away the pressure of shipping as-perfect-as-you-can-get-it code, but still required infrastructure.

Then, the cloud came and eventually became as simple as typing a few keys to spin up a server. Heroku (for those who remember it). And then tons of frameworks and libraries to instantly build stuff. The app explosion. Software dropping in price of production is nothing new. But AI has dropped it even more precipitously. And it’s helped give the software cost-dropping “bug” (har har) to a lot of other industries.

Census data is pretty striking. Americans filed 5.67 million business applications in 2025, a record, and 2026 is running ahead of that pace. Before the pandemic, the monthly rate was roughly 292,000. This May it was 524,000. There have been two distinct legs up: one starting mid-2020 and a second one starting mid-2025.

Now, before we get carried away, let’s poke at some of the holes in this argument. The surge started in mid-2020—two and a half years before ChatGPT existed—so the original driver was the pandemic reshuffle (remote work, stimulus checks, and the quits wave), not AI. That differential in 2020 is obviously not driven by LLMs. And most business applications never become businesses in any meaningful sense.

So how should we interpret this? Is it all fluff? No. Actual establishment births—real businesses, physically forming—are running about 45% above the pre-pandemic rate. John Haltiwanger, the economist who spent two decades documenting the decline of American dynamism and has every professional incentive to be dour about this, conceded that there is indeed a lot of true business formation. The Economic Innovation Group calls it the largest increase in American economic dynamism in at least 30 years.

Despite a lot of folks saying it’s a bubble (and I’ve said myself that stock prices are likely unsustainably high), the US economy is genuinely booming. And although it’s hard to perfectly attribute to AI, my own observations have suggested that it certainly helps. A lot.

Which brings me to what I’m seeing firsthand.

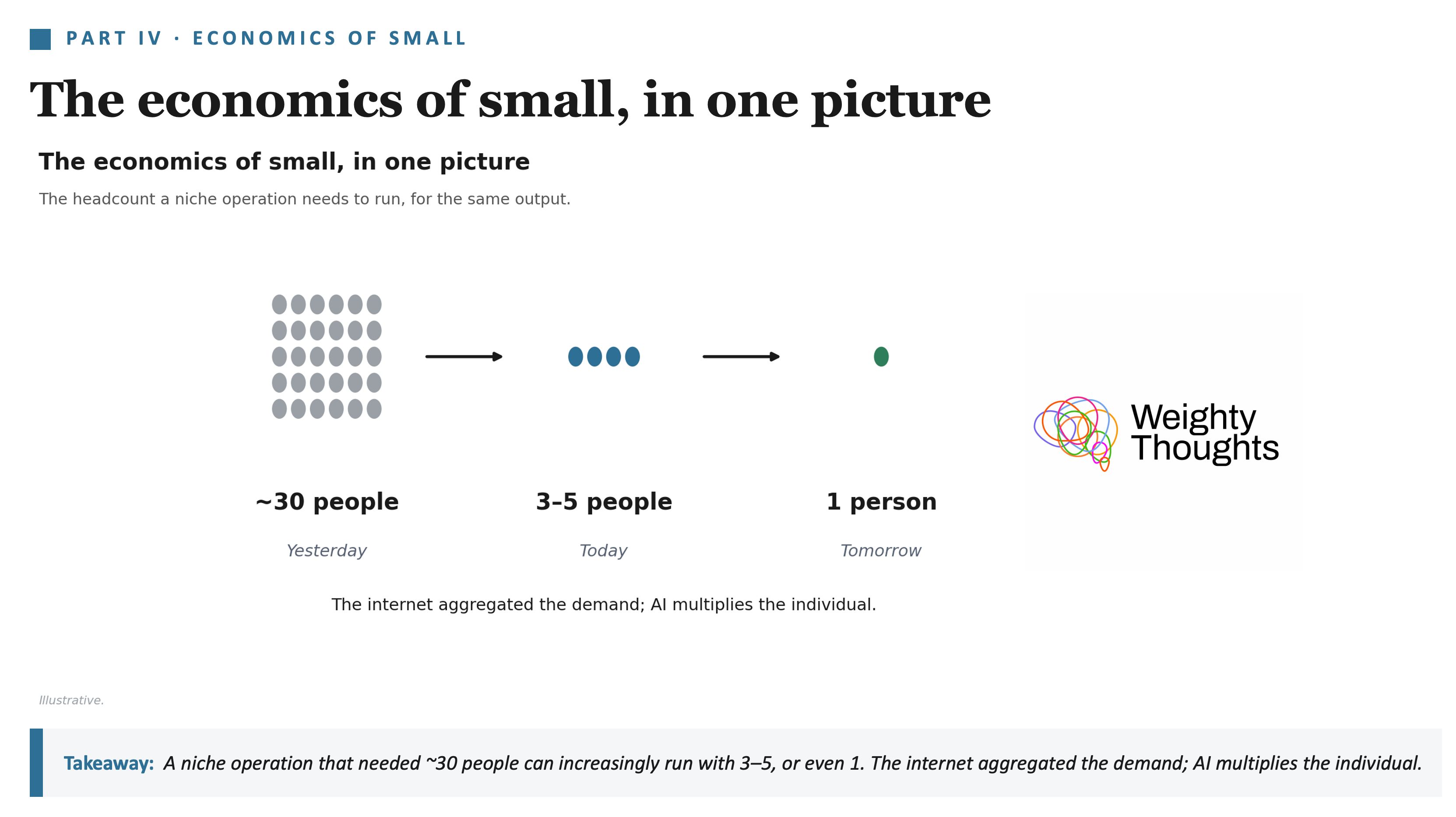

Three People, Eight-Figure Revenue

I currently know of nearly twenty companies running somewhere between $10 million and $100 million in annual recurring revenue with three to five people. Not fifty or a hundred people. Three to five. A few have grown a bit (“teens” of people) since I first came across them, but they remain absurdly small relative to the amount of business they execute.

And no, these are not startups or venture-backed companies. They likely never will be. They are probably capped near where they are—but that’s pretty good given their size. They are spread across finance, healthcare, e-commerce, and more.

These companies—I almost just want to call them “teams”—won’t be behemoths… but “not behemoths” is most of the economy and what employs most people. They don’t raise splashy rounds, because they don’t need to. They also don’t need to do a bunch of press releases touting how much they can do, which is what a company that wants funding would do. These companies don’t particularly want to put a neon sign on top of their quiet niches.

The famous public example is The New York Times piece from April: “How A.I. Helped One Man (and His Brother) Build a $1.8 Billion Company,” about Medvi, a two-employee online company selling GLP-1s.

Now, do note, it didn’t survive contact with scrutiny. The $1.8 billion was a revenue projection, the FDA had sent the company a warning letter six weeks before the article ran, and reporters subsequently surfaced AI-generated “doctor” personas pushing its ads (though, I suppose, the last one is partly how they’re leveraging AI)—after which the Times appended an editors’ note.

Still… while it isn’t $1.8B, Business Insider reported that Medvi had $401mm in revenue and $65mm in profit in 2025. That’s far from a totally fake “AI can allow you to have a tiny company with huge revenue,” even if the headline numbers overstated it.

Most of the around twenty companies I’m referring to? They’re going after regional or small business niches that otherwise have companies of a few hundred or thousand people. That will be disruptive, but we may also get a thousand flowers blooming all over the place in all kinds of niches that were previously too small to sustain businesses.

The internet aggregated people to allow tiny niches (say, random fandoms) to buy merch from Shopify stores, where even the biggest cities in the world wouldn’t sustain a physical store for it. Now, that random Shopify store might literally need only one person where it used to need ten—which further drives down the cost and expands the scope of what’s viable.

Ok, now let’s get back to America. The giants don’t get to stay giants.

Alexis de Tocqueville, touring the United States in the 1830s, wrote what still might be the best description of the American economic personality:

“In the United States a man builds a house to spend his latter years in it, and he sells it before the roof is on: he plants a garden, and lets it just as the trees are coming into bearing: he brings a field into tillage, and leaves other men to gather the crops: he embraces a profession, and gives it up.”

He was describing farmers. It obviously scaled.

(Speaking of farmers, in terms of creative destruction: agriculture went from about 40% of American jobs in 1900 to under 2% today, and I don’t hear many people complaining that ever since we had fewer farmers, no one has had a job…)

In 1980, the most valuable company in America was IBM, and seven of the top ten were oil and gas companies. Not one of the ten was founded after World War II. At the end of 1999, near the dot-com era’s height, the most valuable was Microsoft, at $604 billion—and of that top ten, Microsoft is the only one still in it today. As of this week, nine of America’s ten most valuable companies were founded in 1975 or later. The sixth most valuable, SpaceX, was founded in 2002 and has been publicly traded for all of three weeks. These six, as we covered, sit at the very top of the world list.

Retail tells the same story. A&P was the Amazon of the 1930s—the largest retailer on the planet. Sears displaced it, and by 1969 Sears alone accounted for roughly 1% of the entire US economy. Walmart took the crown in 1991, and Sears filed for bankruptcy in 2018. Amazon passed Walmart in market value in 2015 while generating a fifth of Walmart’s revenue. And Walmart, notably, refused to play its assigned role as the corpse: it rebuilt itself into an e-commerce company and sits near record highs today. Sears died. Walmart adapted. Amazon rose.

Now, IBM never died either—it’s actually at an all-time high this summer on the quantum computing rally, which is kind of funny. But the company that once was computing is now about 1/18th the value of a single company selling GPUs (albeit an important one!). Of the original 1955 Fortune 500, 52 remain on the list. The average tenure of an S&P 500 company has fallen from about 33 years in the 1960s to roughly 15 today.

Reeling back the flag-waving, which I normally don’t really engage in (but I’ll make an exception for the 4th of July)… American churn has slowed after 2000. While recent business formation has boomed, one will notice that big American firms aren’t falling dead quite as rapidly as they did before.

From 1980 through the 2010s, American dynamism declined—economists wrote paper after paper documenting falling startup rates, rising concentration, and aging firms. The same seven companies sat on top of the market from roughly 2010 to 2024, and they are currently spending north of $700 billion a year on AI infrastructure—which you can read as capex, a colossal waste of money, or… the most expensive moat in commercial history.

While I do think a lot of middle businesses are going to be disrupted by new businesses, there is a possibility that we will have slower turnover at the top, especially if they find ways to entrench themselves. And, of course, one of the best ways is to become regulated as the “safe” options, maybe even under the guise of national security (cough OpenAI and Anthropic cough)… anyway, a rant for another day, but I bring it up since it is useful to point out that there may be a counterforce there.

National Champions vs. Temporary Winners

As I’ve alluded to, other economies tend to have a lot more… permanence.

Mario Draghi, in his competitiveness report to the EU: “There is no EU company with a market capitalisation over EUR 100 billion that has been set up from scratch in the last fifty years. All six US companies with valuations above EUR 1 trillion have been created in that period of time.” One can obviously get a flavor of it from the companies I mentioned in the introduction.

This isn’t because Europeans can’t build new things: Lovable, ElevenLabs, Mistral, and DeepMind-before-Google all say otherwise. Europe starts companies. It just can’t seem to let them get big or let the old ones make room. I’ve written before about the EU’s regulatory instincts, and my view hasn’t changed. European people are great. Its policy architecture is terrible.

Asia has its own model that is quite different, of course.

Japan ran the strongest version of a national champion model (before China). In 1989, four of the five most valuable companies in the world were Japanese banks. The #1, Industrial Bank of Japan, no longer exists. Of that era’s corporate elite, only one—Toyota—remains in Japan’s top ten under its own name. Toyota just lost the top spot last month to Kioxia, a memory chip maker riding the AI boom (a NAND cousin of Micron, at a fraction of the size, but subject to the same memory boom!). It’s not a “new” company, though. Kioxia is a carve-out of Toshiba, founded in 1875. Perhaps one way of saying it is Japan churns names, not bloodlines (in some ways, semi-literally with zaibatsu).

Korea is similar: every top chaebol dates from 1938 to 1953, and Samsung plus SK Hynix alone are over half of the entire KOSPI. Taiwan as a modern entity is simply younger. TSMC (1987) is a genuinely new global champion, but it’s the Taiwanese champion that sucks all of the air (and talent) away from the rest.

As Ben Thompson from Stratechery has argued in various forms (see “Microsoft’s Monopoly Hangover” or “The End of the Beginning”), new companies that become big don’t tend to just do that. They need old ones to get out of the way. Other countries don’t do this particularly well.

China, of course, is not stagnant. It’s not a young country, but its modern reemergence is fairly recent.

ByteDance is fourteen years old and worth over half a trillion dollars. DeepSeek is three. Chinese domestic competition is so ferocious that the median net margin across 33 listed automakers fell to 0.83%, a bloodbath the government literally calls “involution.” As such, it’s complicated… because I’m not sure anyone would describe the Chinese ecosystem as a free-flowing ecosystem of companies turning over. Seven of the ten most valuable listed companies are state-controlled banks and energy firms. When internal competition and price wars got too destructive (I promise you, Chinese EVs, for example, were not competing so hard because of US/European firms…), Xi personally chaired the meeting ordering companies to stop competing so hard.

The US is a free-for-all, a survival of the fittest. And while that sounds cruel, we shouldn’t care about companies. Which I never thought would be that hard of a concept for people to understand—we have so many vague comments about how “corporations are bad” these days. We should care about people and people thrive when there’s turnover (creative destruction!), and these exact corporations cannot accumulate power for too long. Because they die.

A quick rant: This is something we shouldn’t lose in the US! Since early 2025, the federal government has taken about $21 billion in direct equity stakes across 16 companies. It is now Intel’s largest shareholder. The Pentagon is the largest shareholder of our rare-earth champion, complete with a ten-year guaranteed price floor. A golden share in US Steel was exercised to stop a plant from closing. The government takes a 15% cut of certain AI chip sales made by Nvidia and AMD to China. Are these for national security? Are they just a grift from our current somewhat (potentially very) corrupt administration? Maybe yes to all, but it’s worrisome either way. (And yes, I know the Intel stake is up hugely on paper. That’s not the point—the point is what a government-backed champion does to everyone who might otherwise replace it.)

Protect People, Not Companies

Young firms create essentially all net new American jobs: about 2.9 million a year, against 1.4 million for the entire private sector combined, meaning that without startups, net US job creation would be negative.

By the way, America’s real edge isn’t starting companies—several European countries have higher firm entry rates than we do. As said, Europe doesn’t have a problem starting companies. The edge is up-or-out. Since you already have heard about the top six companies a few times already, let’s give a broader real economy example. A forty-year-old American plant employs roughly eight times what it did when young/new; in India and Mexico the figure is about two. That’s an example of how companies that are allowed, encouraged… or forced… to grow, hire. Companies that are merely preserved don’t.

Of course, when companies die, they start shedding workers. I’m not saying there’s no disruption, especially in the short term. But it keeps everything long-term healthier—which I think is the story of AI as well.

This can even be extended to a (specific) European context. Denmark runs one of the most brutally Darwinian firm-level economies in the world—easy hiring, easy firing, minimal corporate protection. Of course, it’s still Europe. This is paired with roughly two years of unemployment support and aggressive retraining. They get the dynamism, and people land on their feet. (This is a policy I don’t mind at all—and probably one the US needs to get better at.)

Protect companies and you will almost always hurt the aggregate of people. We shouldn’t care about companies. It’s about the people.

At 250

The US is far from perfect. I think that’s a… well, far more obvious thing to say, especially very recently (cough Iran cough). Nevertheless, the Declaration of Independence, at 250 years old, is not a document of achievement. The men who signed it obviously failed to live up to it the moment ink hit parchment. “All men are created equal” is quite a thing to say when chattel slavery of Africans existed and wouldn’t be overturned without a bloody Civil War (and would still have institutions persist far after). I guess at least it’s “men,” so women not having the vote until 1920 isn’t quite as stark a hypocrisy… but only technically.

America is not really about meeting all of its ideals—which it never has. It’s about striving towards it and eventually correcting it. It is still, despite all of the political backlash to immigration (which, to be fair, goes far beyond the US), one of the few true nations of immigrants in the world, and obviously the biggest by far.

Tocqueville said when the nation was 59: “The great privilege of the Americans does not simply consist in their being more enlightened than other nations, but in their being able to repair the faults they may commit.”

We do so in government. And we’ve done so in our economy. And I hope we keep doing so, with the AI disruption and beyond. Because, ultimately, I think the biggest beneficiaries of AI will be people (I’ve said before that I think most of the economic surplus will be socialized—which doesn’t mean socialism; it just means the welfare benefits will be distributed widely and not captured by companies as profits).

Happy 250th to the United States—and here’s hoping it keeps the soul that brought it this far.

Thanks for reading!

I hope you enjoyed this article. If you’d like to learn more about AI’s past, present, and future in an easy-to-understand way, I’ve published a book titled What You Need to Know About AI.

You can order the book on Amazon, Barnes & Noble, Bookshop, or pick up a copy in-person at a local bookstore.

What a great article. Some very interesting stats in many areas. Nice job!