Oil, Iran, and AI's Energy Problem?

Why the Biggest Oil Shock in Modern History Isn't Threatening US Datacenters (So Far)

“Oil’s price spike is bad news for power-hungry AI.” “The Iran Conflict Is Quietly Reshaping the AI Trade.” “How War in Iran Could Cripple the Global Digital Economy.”

If you’ve been nodding to these headlines, I get it. Oil prices are surging. AI runs on energy. It feels right—especially if you’ve been wincing at the gas pump every time you fill up your car. That visceral, twice-a-week reminder that energy prices are spiking is hard to ignore, and it’s natural to assume it ripples into everything. And that’s why it’s great to explain why that’s wrong—or, at least, it’s more nuanced than that.

We’re back to our regularly scheduled programming, especially now that the Iran situation is clearly more involved than the quick in-and-out that Venezuela ended up being. As usual, Jordan Schneider has good content on the geopolitics/military situation, but I’m talking about the implications for datacenters here.

So, why is the gut-feel narrative wrong, or at least not right?

Oil, natural gas, and electricity are three different commodities with three different supply chains, three different price dynamics, and three very different relationships to the Middle East. Conflating them—treating “energy” as one fungible thing—leads to bad analysis. It’s also, incidentally, the kind of confusion that commodity traders and macro funds get paid to exploit. Understanding the actual linkages, even (especially) when they defy intuition, is how you make money in markets. And in this case, the intuition is wrong. At least for US and Chinese datacenters (... it’s more complicated elsewhere).

Let’s talk about it.

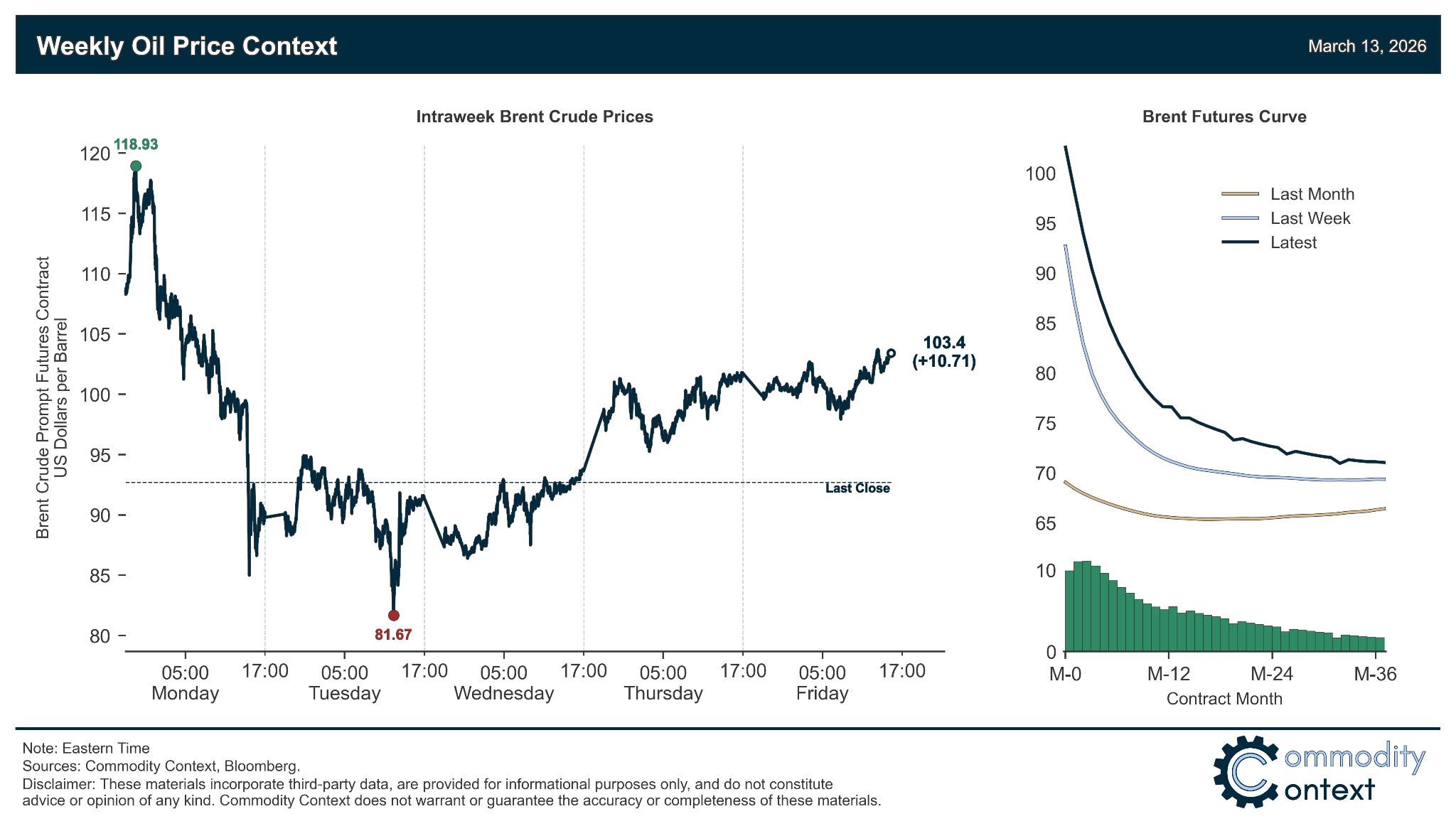

First, the context. On February 28th, the United States and Israel launched roughly 900 coordinated strikes against Iran. Iran’s Supreme Leader was killed. Iran responded by threatening—and then largely succeeding in practicality—a blockade of the Strait of Hormuz. Shipping through the strait all but ground to a halt—Kpler estimated tanker transits down ~92% versus the prior week, with daily passages falling from 37 pre-war to near zero within days. Brent crude peaked near $120 a barrel. Qatar’s largest LNG export facility was hit by an Iranian drone and shut down. 400 million barrels were released from emergency petroleum reserves—the largest release in history.

This is the biggest oil supply disruption in modern history. The Strait of Hormuz handles about 20% of global oil supply and roughly a quarter of all seaborne oil trade. For context: the 1973 Arab oil embargo disrupted about 9% of global supply. The 1979 Iranian Revolution disrupted roughly 4%. The Gulf War in 1990, about 6%. Russia-Ukraine in 2022, roughly 3%. This crisis dwarfs all of them. (As Paul Krugman recently detailed, the historical comparisons are not great for this being something global supply chains can paper over.)

So yes, this is serious. Separately, I’m not dismissing the geopolitical crisis or its humanitarian toll. But you can get that side of things from plenty of places. We’re talking about technology and markets, so let me talk about the part that’s more my bailiwick: the claim that this is an AI infrastructure problem.

It isn’t. At least not yet. And understanding why it isn’t—getting past the vibes and into the actual plumbing of energy markets—is more useful than the panic.

Oil Is Not Electricity

Let’s start with the most important fact that makes “oil shock kills AI” largely wrong:

Petroleum provides less than 1% of US electricity generation. Less than half a percent, actually—petroleum liquids and petroleum coke together account for roughly 0.3–0.4% of total US generation.

The US electricity grid runs on natural gas (~43%), renewables (~23%), nuclear (~18%), and coal (~15%). Oil is used for transportation—gasoline, diesel, and jet fuel. It powers your car, not datacenters—and hence not your ChatGPT queries.

When Brent crude hits $120 a barrel, that’s a crisis at the gas pump. It is not, in any direct sense, a crisis for the US power grid. The reason you feel like energy prices are exploding is because you interact with gasoline twice a week. It’s the most visible energy price in your life. And, hence, a serious problem for politicians. But it’s not the price that matters for datacenters.

The gap between those two things is the entire point of this article.

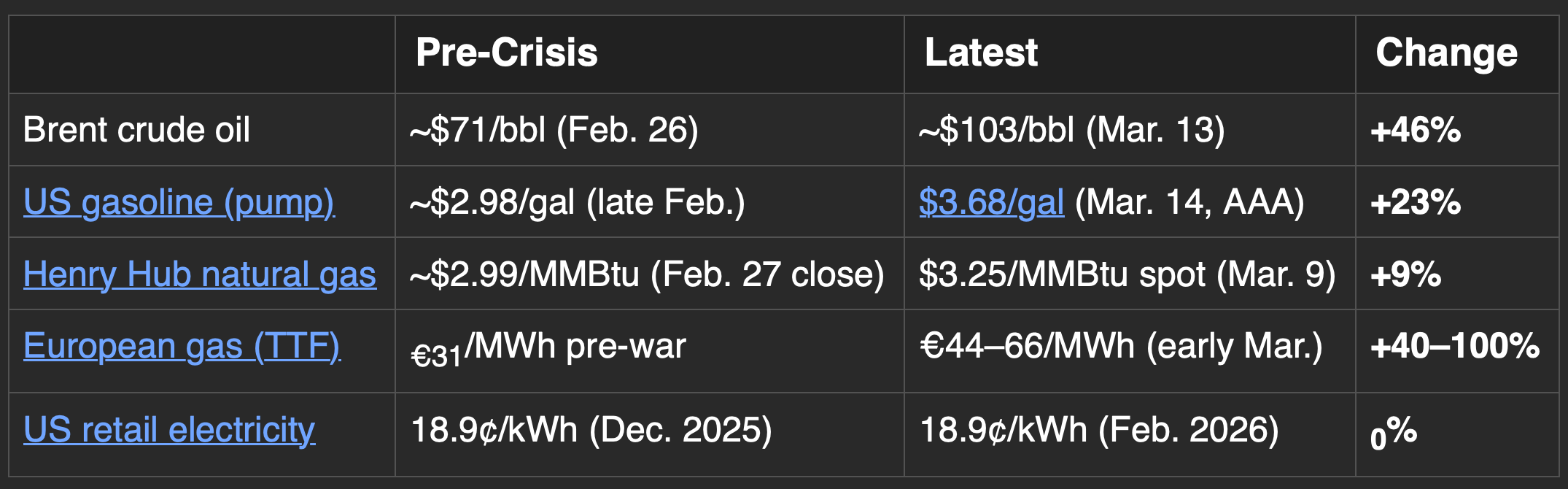

Fortunately, we don’t need to argue this theoretically, because the Iran crisis has given us a beautiful natural experiment. Here’s what happened to various energy prices since the strikes began:

Note: Oil and gas figures are daily spot prices; US retail electricity is the BLS/CPI national average price, a monthly figure that lags by several weeks. The comparison across different data frequencies is imperfect—but the magnitude of the gap is the point. Even if the broad retail indicator hasn’t budged, there’s no evidence yet of a generalized electricity-price shock propagating from crude. Brent also briefly spiked past $119 on March 10 before losing altitude again.

Oil surged. Gasoline jumped. European gas spiked. US electricity didn’t move.

In a way, I could end the article here. The table basically shows my whole argument. So, let’s see if we can try to steelman the “oil crisis destroys AI” argument a bit more.

“But natural gas and oil are correlated!” That’s more or less the load-bearing argument for most of the articles. The thing is, they’re really not. Not anymore. CME Group research shows oil and gas prices have been largely decoupled since around 2008. They overlap mainly during periods when broad macroeconomic forces hit both markets simultaneously—which isn’t what’s happening here. This is a specific regional supply disruption, not a global demand shock.

The reason US natural gas barely moved while European gas doubled is straightforward: the US has been a net gas exporter since 2017. Our LNG export terminals are already running at full capacity, so there’s no mechanism for surging global LNG demand to suddenly drain our domestic supply. As Axios put it, “America’s natural gas bounty is acting like a moat, largely shielding the U.S. from price spikes while much of the world reels.” The gas powering Virginia’s datacenters and Texas’s ERCOT grid comes from American shale, not the Strait of Hormuz.

Natural gas is hard to move around. Commodities are not like digital bits and can’t be instantly transmitted, despite the miracle of the modern supply chain. Heck, not even oil is totally fungible—remember all of the challenges for sweet, light crude versus sour, heavy crude (Venezuela) for refining. West Texas Intermediate (WTI) and Brent, two global oil benchmarks, can diverge dramatically at times.

One last helpful illustration: Hawaii. It’s the only US state that actually burns oil for electricity in meaningful quantities—and pays far above the national average for the privilege, roughly 40¢/kWh or more than 2x what the mainland pays. Hawaii proves the mechanism works. If you’re oil-dependent for power, oil prices matter enormously. The continental United States simply isn’t. We aren’t yet seeing Hawaiians screaming, but rates are set monthly... and it could look ugly next month.

Though, let’s now reel my argument back a bit: the crisis is two weeks old. If the conflict persists for months and global LNG competition eventually bids up Henry Hub meaningfully, this picture could shift. Chatham House notes that US energy prices were already trending up before Iran—driven by domestic demand from (among other things) datacenters. But as of mid-March 2026, the data is not ambiguous. The biggest oil shock in modern history has not yet shown up as a comparable surge in US retail electricity prices, which remain driven far more by domestic power-market structure and natural-gas dynamics than by crude itself.

Where It Actually Matters

The rest of the world is not so lucky. And this is where it gets genuinely interesting for anyone thinking about the global AI infrastructure buildout—not just the American one.

The Middle East: Datacenters as Military Targets

This one’s obvious in hindsight but was apparently not obvious to the people who spent billions building cloud infrastructure in the Gulf. Iranian drones hit three AWS datacenters—two in the UAE, one in Bahrain—in the first days of the conflict. AWS reported“structural damage” and “disrupted power delivery to our infrastructure.” Banking apps went down across the region. Enterprise software broke.

I wrote last year about how AI is overturning the military world order. Datacenters are strategic infrastructure now, and they got treated as such. Iran has reportedly identified dozens of datacenter locations across the Gulf for potential targeting—Amazon, Microsoft, IBM, Google, Oracle facilities. The $20 billion first phase of the Stargate UAE project (OpenAI, Oracle, NVIDIA) sits in Abu Dhabi, with plans for a 5 GW campus. Looked great before—now it’s a war zone.

And here’s the key difference from the US: Gulf states actually do burn oil and gas for electricity. Saudi Arabia’s grid is nearly entirely fossil fuel-dependent. This is not the US grid. When crude doubles, their power costs go up in a way ours simply don’t. They could always control it through decreasing exports and simply capping prices, but someone pays the piper. If they do it, the government is just absorbing the cost.

Europe: The LNG Shock

Europe is exposed because Europe is dependent on imported natural gas for a meaningful share of its electricity generation. Qatar supplies roughly 20% of global LNG, and the vast majority transits through Hormuz. When that supply shut down, European gas prices on the TTF benchmark surged 45–70%. Again, in a crisis, it’s very clear commodities in different places are not totally fungible. They don’t magically teleport to where they’re needed.

Worse, Europe entered 2026 with gas storage well below recent years—a structural vulnerability that existed before this crisis started. As Rory Johnston at Commodity Context has been writing and illustrating well, there’s “no end in sight” for the energy pressure.

The deeper issue for European AI infrastructure: Europe was planning to add substantial new gas generation capacity partly to service growing datacenter demand. They’re locking themselves into gas dependence at the exact moment gas became expensive and unreliable. Ireland is a particularly stark example—Irish datacenters already consumed 22% of the country’s metered electricity in 2024, and instead of going green, many are increasing gas consumption.

This is, of course, the same Europe that shuttered a bunch of nuclear power plants for greater reliance on Russian gas (despite all of the green rhetoric) right before the Russian invasion of Ukraine... Either from luck or poor decision-making, they’ve just continuously been in a terrible position for energy (and for a lot of other things).

Asia: The Import Dependency Trap

Japan gets the vast majority of its oil and a significant share of its LNG through Hormuz. South Korea is similarly exposed. Singapore’s refineries cut operations by 40–50%. These are major economies with growing datacenter sectors, and they’re acutely vulnerable to exactly this kind of disruption.

China: The Quiet Winner

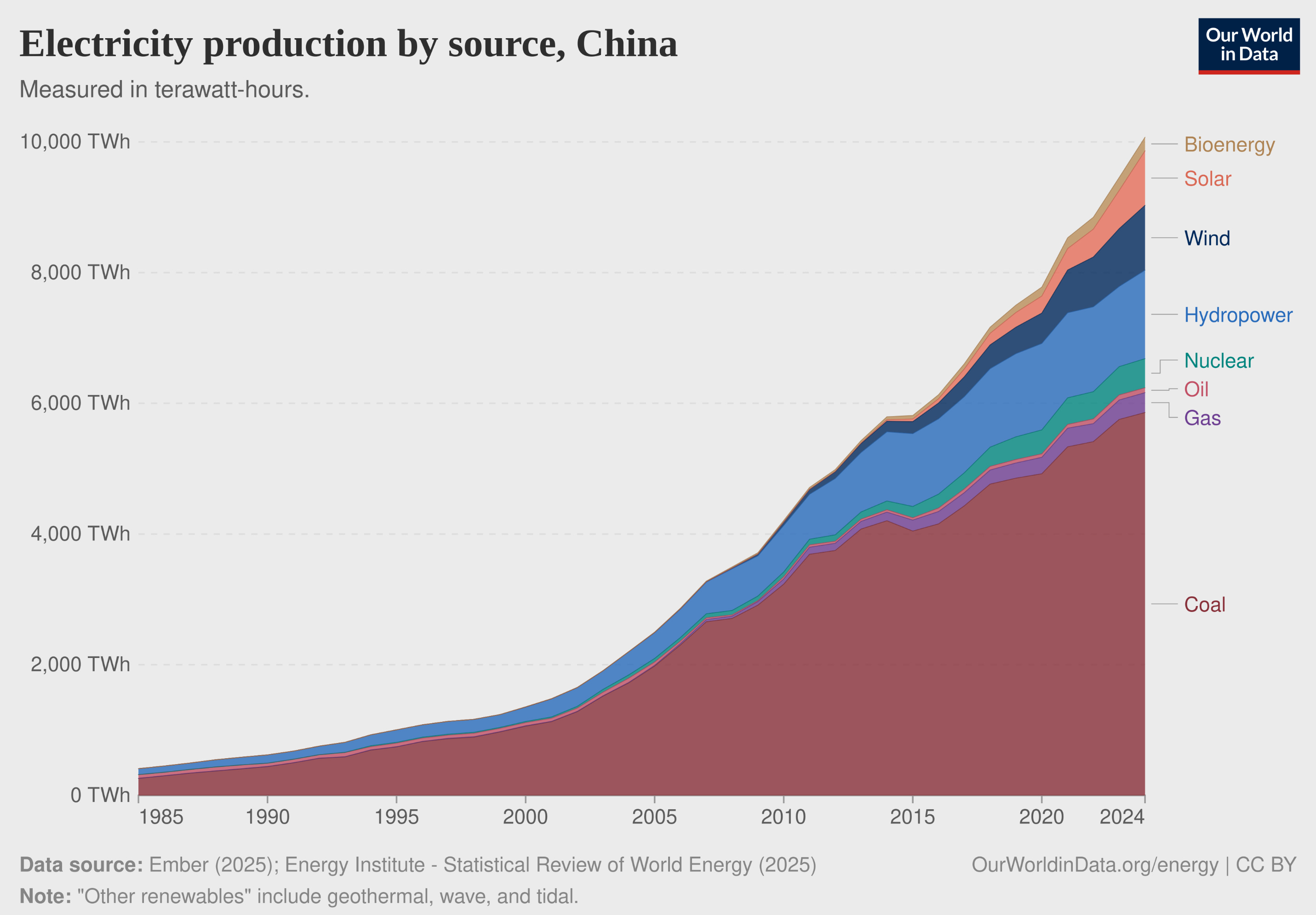

Finally, there’s China. Oil and natural gas account for only ~3% of China’s power mix—natural gas alone was just 2.8% of China’s electricity network in 2025. The grid runs on coal (still the baseload backbone) and renewables (whose growth met ~84% of China’s electricity demand growth in 2024). China’s clean energy capacity reached 52% of total installed capacity by February 2026—1,494 GW clean versus 1,420 GW fossil—a milestone, though generation still lags behind capacity since renewables have lower utilization rates than fossil plants.

As Grace Shao has discussed before, China may be lagging in chip and datacenter (space) efficiency, but they’re making up for it in part with a massive energy buildout. While the US debates permitting for new gas plants and nuclear restarts, China has been adding capacity (both coal and renewable) at a staggering pace. Their AI infrastructure is structurally insulated from Middle East disruptions in a way that Europe and much of Asia are not. The Oxford Institute for Energy Studies published an interesting paper on this in February (before the war even started) titled “The China Data Centre Advantage: Hype Versus Reality.”

I’ve written before about who’s winning the AI war. Everyone was talking about power capacity. Energy security wasn’t really part of that calculus until two weeks ago. I expect that’s changed now.

Now, how much does this global differential actually matter?

Honestly, less than the headlines suggest for any individual company in the near term. The hyperscalers have been hedging geographic risk for years—Microsoft, Meta, and Google all have nuclear power deals that, while still years away from delivering power, signal awareness that fossil fuel dependency is a strategic vulnerability. And the datacenter industry is, by nature, designed to route around damage—that’s the whole point of multiple availability zones. So, I don’t expect there to be wholesale abandonment of Middle Eastern datacenters.

But in aggregate, over a multi-year buildout involving ~$650–690 billion in annual hyperscaler capex (depending on the analyst aggregation)? The question of where you build matters a lot (I’d argue it’s always mattered, but people don’t take some of these risks into account until forced).

Hyperscalers are already slowing new capital deployments in the Gulf and considering accelerated projects in Northern Europe, India, and Southeast Asia. Again, not wholesale abandonment, but the war is reshaping the geography of AI infrastructure in real time.

What Actually Threatens the US AI Buildout

So if the Iran crisis isn’t the thing to worry about for US AI infrastructure, what is?

The answer is a lot less dramatic than a war but a lot more grinding. It’s also the same one it was before. Last November, my former Bridgewater colleague Josh Blanchfield wrote a guest post here arguing—convincingly, I think—that AI’s power requirements aren’t intractable. His main point was that the energy exists; the question is whether we can mobilize it fast enough. I agree. But “fast enough” is doing a lot of work in that sentence, because the real chokepoints are all about speed—and they’re mostly the boring kind:

Grid interconnection queues. In PJM (a “regional transmission organization,” which covers 65 million people across 13 states), projects that came online in 2025 spent an average of 8 years waiting in the interconnection queue. There are ~2,300 GW of total generation and storage capacity seeking connection—nearly 2x the entire installed US fleet. You want to build a datacenter? Great! Get in line. A very long line.

Local opposition. Between May 2024 and March 2025, $64 billion in datacenter projects were blocked or delayed by local opposition. By Q2 2025, that hit ~$100 billion in a single quarter. Only 44% of Americans would welcome a datacenter nearby—less popular than gas plants, wind farms, or even nuclear facilities. Datacenters are somehow less popular than nuclear power plants. Funny that something finally beat nuclear plants in a NIMBY-hate-contest.

Power transformer shortages. Large power transformers have 2.5–4 year lead times. The US faces a 30% supply deficit, with unit costs up 77% since 2019. The US relies on a single domestic supplier of grain-oriented electrical steel. No meaningful relief before 2027.

Water. US datacenters could require 697 million to 1.45 billion additional gallons per day by 2030—equivalent to New York City’s daily water supply. That’s water for cooling, not for drinking, but try explaining that distinction to the residents near a proposed facility (see: local opposition, above).

Gas turbine lead times. Even though natural gas is abundant and cheap, the equipment to burn it has 5–7 year lead times for large-frame units, up from 2 years in 2021. The fuel isn’t the bottleneck. The hardware is.

No one writes breathless articles about transformer lead times or interconnection queue backlogs. But these are the actual binding constraints on whether the US AI buildout hits its timeline. As I argued in “Shortages Create Opportunity”—this is the same framework. The constraints create openings for whoever solves them.

However, the constraint needs to live long enough to actually put capital to work and invent new startups/technology to tackle it. One of the issues here is how long will this Iran situation persist? No one knows. I suspect not even the White House or Iranian leadership knows.

The Real Macro Risk

Now, if I were going to connect the Iran crisis to the AI buildout, the transmission mechanism isn’t oil→electricity. It’s oil→recession→capex cuts. That’s the channel that should actually keep people up at night.

The top hyperscalers are projected to spend ~$650–690 billion in 2026 capex, with something like 90% of operating cash flow going to capital expenditure (up from a 10-year average of 40%). AI infrastructure investment has become a significant driver of US GDP growth—without it, the economy would look a lot weaker.

If $120 oil tips the US economy—and oil shocks have a pretty solid track record of doing exactly that—the question isn’t “can we afford the electricity?” It’s “do CFOs keep signing off on $200 billion annual datacenter budgets during a downturn?” Microsoft’s management has signaled that meaningful cash returns from GenAI may lag infrastructure deployments by a year or two—the kind of caveat that becomes a problem when revenue growth slows.

I’ve argued before that the AI bubble will burst eventually—not because AI isn’t real, but because technology bubbles always reflect real technologies whose market prices ran ahead of reality. An oil-induced recession would be an exogenous shock, not a reflection of AI’s fundamentals. But markets don’t much care about the distinction when they’re repricing risk.

So What?

The Iran war is the biggest oil supply disruption in modern history. It is a real crisis—for drivers at the pump, for European energy security, for Gulf states whose datacenters are literally being hit by drones, and for Asian economies dependent on Middle Eastern fuel.

But for American AI datacenters? Oil is not electricity. Gas is not oil. And the data from the last two weeks proves it: crude up 46%, US electricity flat.

Energy security matters for the global AI buildout—but it matters differently depending on where you are. The US and China are insulated, for entirely different reasons. Europe and Asia are exposed. And the Gulf states just learned that “strategic infrastructure” becomes “strategic target” rather quickly.

Think less about the price of oil and more about the 8-year queue to plug into the grid.

Thanks for reading!

I hope you enjoyed this article. If you’d like to learn more about AI’s past, present, and future in an easy-to-understand way, I’ve published a book titled What You Need to Know About AI.

You can order the book on Amazon, Barnes & Noble, Bookshop, or pick up a copy in-person at a local bookstore.